All Categories

Featured

Table of Contents

For lots of people, the biggest issue with the limitless banking principle is that first hit to early liquidity brought on by the prices. This con of infinite financial can be lessened substantially with correct plan design, the initial years will always be the worst years with any kind of Whole Life policy.

That claimed, there are specific unlimited banking life insurance policy plans made primarily for high early cash money value (HECV) of over 90% in the very first year. Nonetheless, the long-lasting performance will certainly commonly considerably lag the best-performing Infinite Financial life insurance policy plans. Having accessibility to that additional 4 figures in the initial couple of years might come at the price of 6-figures down the roadway.

You really obtain some significant long-lasting benefits that aid you recover these early costs and afterwards some. We discover that this prevented early liquidity issue with limitless banking is more mental than anything else when completely checked out. If they absolutely needed every penny of the cash missing from their limitless banking life insurance plan in the first couple of years.

Tag: unlimited banking concept In this episode, I chat about financial resources with Mary Jo Irmen that instructs the Infinite Financial Concept. With the rise of TikTok as an information-sharing platform, financial suggestions and approaches have found a novel way of spreading. One such strategy that has actually been making the rounds is the limitless banking concept, or IBC for short, garnering recommendations from celebs like rapper Waka Flocka Fire.

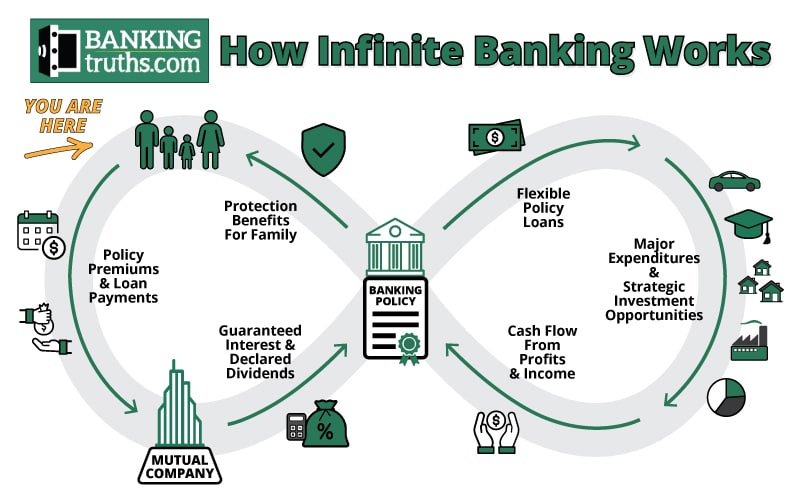

Within these plans, the money value expands based upon a price set by the insurance firm. Once a substantial cash money worth accumulates, policyholders can get a cash worth financing. These finances vary from conventional ones, with life insurance acting as security, suggesting one could lose their protection if loaning exceedingly without adequate cash money value to sustain the insurance policy expenses.

And while the allure of these policies is noticeable, there are inherent limitations and threats, necessitating attentive cash money value tracking. The strategy's legitimacy isn't black and white. For high-net-worth people or local business owner, particularly those utilizing techniques like company-owned life insurance coverage (COLI), the benefits of tax obligation breaks and substance growth could be appealing.

Bioshock Infinite Vox Cipher Bank

The attraction of unlimited financial doesn't negate its obstacles: Expense: The fundamental need, a permanent life insurance coverage plan, is pricier than its term equivalents. Eligibility: Not everybody gets approved for whole life insurance coverage due to rigorous underwriting processes that can leave out those with specific wellness or way of living problems. Intricacy and danger: The complex nature of IBC, combined with its risks, might hinder many, specifically when simpler and much less risky alternatives are readily available.

Assigning around 10% of your monthly earnings to the policy is simply not feasible for a lot of people. Part of what you review below is just a reiteration of what has actually currently been claimed above.

So prior to you obtain on your own right into a scenario you're not gotten ready for, know the complying with initially: Although the concept is typically sold thus, you're not in fact taking a funding from on your own. If that were the case, you would not have to settle it. Rather, you're obtaining from the insurance coverage firm and have to repay it with passion.

Some social media blog posts advise making use of money worth from entire life insurance policy to pay down credit report card financial obligation. When you pay back the car loan, a section of that interest goes to the insurance coverage business.

For the very first a number of years, you'll be repaying the commission. This makes it exceptionally tough for your policy to accumulate value throughout this moment. Whole life insurance costs 5 to 15 times much more than term insurance. The majority of individuals merely can't afford it. So, unless you can manage to pay a few to several hundred dollars for the following years or more, IBC will not work for you.

Whole Life Insurance Bank On Yourself

If you require life insurance, below are some useful pointers to take into consideration: Consider term life insurance. Make sure to shop around for the best rate.

Copyright (c) 2023, Intercom, Inc. () with Booked Typeface Call "Montserrat". This Font Software is accredited under the SIL Open Typeface Certificate, Version 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Reserved Font Style Call "Montserrat". This Font style Software application is accredited under the SIL Open Typeface Certificate, Variation 1.1.Miss to major web content

Infinite Banking Wikipedia

As a certified public accountant specializing in realty investing, I have actually cleaned shoulders with the "Infinite Banking Concept" (IBC) much more times than I can count. I've also talked to professionals on the subject. The primary draw, besides the noticeable life insurance policy benefits, was constantly the idea of developing cash worth within a long-term life insurance coverage plan and borrowing against it.

Certain, that makes feeling. Honestly, I constantly believed that money would certainly be much better spent straight on investments instead than channeling it through a life insurance plan Until I uncovered exactly how IBC could be combined with an Irrevocable Life Insurance Coverage Count On (ILIT) to develop generational wide range. Let's begin with the basics.

Infinite Bank Statements

When you borrow against your policy's cash money worth, there's no set repayment routine, providing you the flexibility to manage the funding on your terms. At the same time, the cash worth remains to grow based on the policy's guarantees and returns. This arrangement allows you to accessibility liquidity without interrupting the long-lasting development of your policy, supplied that the funding and rate of interest are managed sensibly.

The process continues with future generations. As grandchildren are born and mature, the ILIT can acquire life insurance policy policies on their lives as well. The trust after that builds up several policies, each with expanding cash money worths and survivor benefit. With these plans in position, the ILIT successfully ends up being a "Family Bank." Member of the family can take loans from the ILIT, utilizing the money worth of the plans to money financial investments, start services, or cover major expenses.

A vital element of handling this Family Financial institution is making use of the HEMS requirement, which stands for "Health and wellness, Education And Learning, Upkeep, or Support." This standard is typically included in trust arrangements to route the trustee on just how they can distribute funds to recipients. By adhering to the HEMS requirement, the depend on makes sure that distributions are made for vital requirements and long-term support, securing the trust fund's assets while still providing for member of the family.

Enhanced Adaptability: Unlike stiff financial institution financings, you manage the repayment terms when borrowing from your very own plan. This permits you to framework settlements in a manner that lines up with your business money circulation. the infinite banking system. Better Capital: By funding service expenses through plan lendings, you can potentially maximize cash money that would certainly or else be bound in standard funding repayments or equipment leases

He has the same equipment, but has actually additionally built extra cash money value in his policy and got tax benefits. And also, he currently has $50,000 readily available in his plan to use for future chances or costs. Despite its prospective advantages, some people remain doubtful of the Infinite Banking Concept. Let's attend to a couple of usual issues: "Isn't this simply costly life insurance policy?" While it holds true that the costs for an appropriately structured whole life policy might be more than term insurance policy, it is necessary to see it as greater than simply life insurance policy.

Infinite Banking Concepts

It has to do with developing a versatile funding system that provides you control and supplies several benefits. When used strategically, it can complement other financial investments and service methods. If you're interested by the possibility of the Infinite Banking Principle for your company, right here are some steps to think about: Enlighten Yourself: Dive much deeper into the principle through reputable books, workshops, or assessments with well-informed professionals.

{kind=link}

Latest Posts

Infinite Banking Concept Life Insurance

Infinite Income System

Infinite Banking Concept Book